The combination of big data and blockchain can significantly improve the usability of each other, and these technologies can help create a hybrid infrastructure with big data and blockchain as the backbone. The infrastructure will be flexible for different application types, such as its parents - big data and blockchain.

It is well known that big data and blockchain can work well together by providing more security and integrity. One is changing data management and the other is completely changing the nature of transactions. Can they have a greater impact on the industry through the combination of big data and blockchain.

Big Data technology first emerged at the turn of the century to meet the computational demands of large data sets in the Internet age. Proprietary applications such as Google’s BigTable and Yahoo’s ZooKeeper demonstrate the potential of big data. However, its potential could only be tapped once open source projects such as the Hadoop file system and Hadoop Map Reduce entered the market. Since then, Big Data has snowballed, changing the way businesses manage data in the 21st century.

An anonymous and mysterious figure introduced the world to blockchain in 2008. It was developed to solve the problem of double spending in transactions by eliminating the need for third parties in financial transactions. Blockchain also brought the world the first digital cryptocurrency, Bitcoin. Since then, the concept of blockchain has grown rapidly, providing a powerful solution to an ongoing problem in many industries. Since both big data and blockchain have been established as effective tools for solving problems in different areas, we look forward to integrating the possible approaches of big data and blockchain to provide better solutions to specific problems.

How Big Data Works with Blockchain

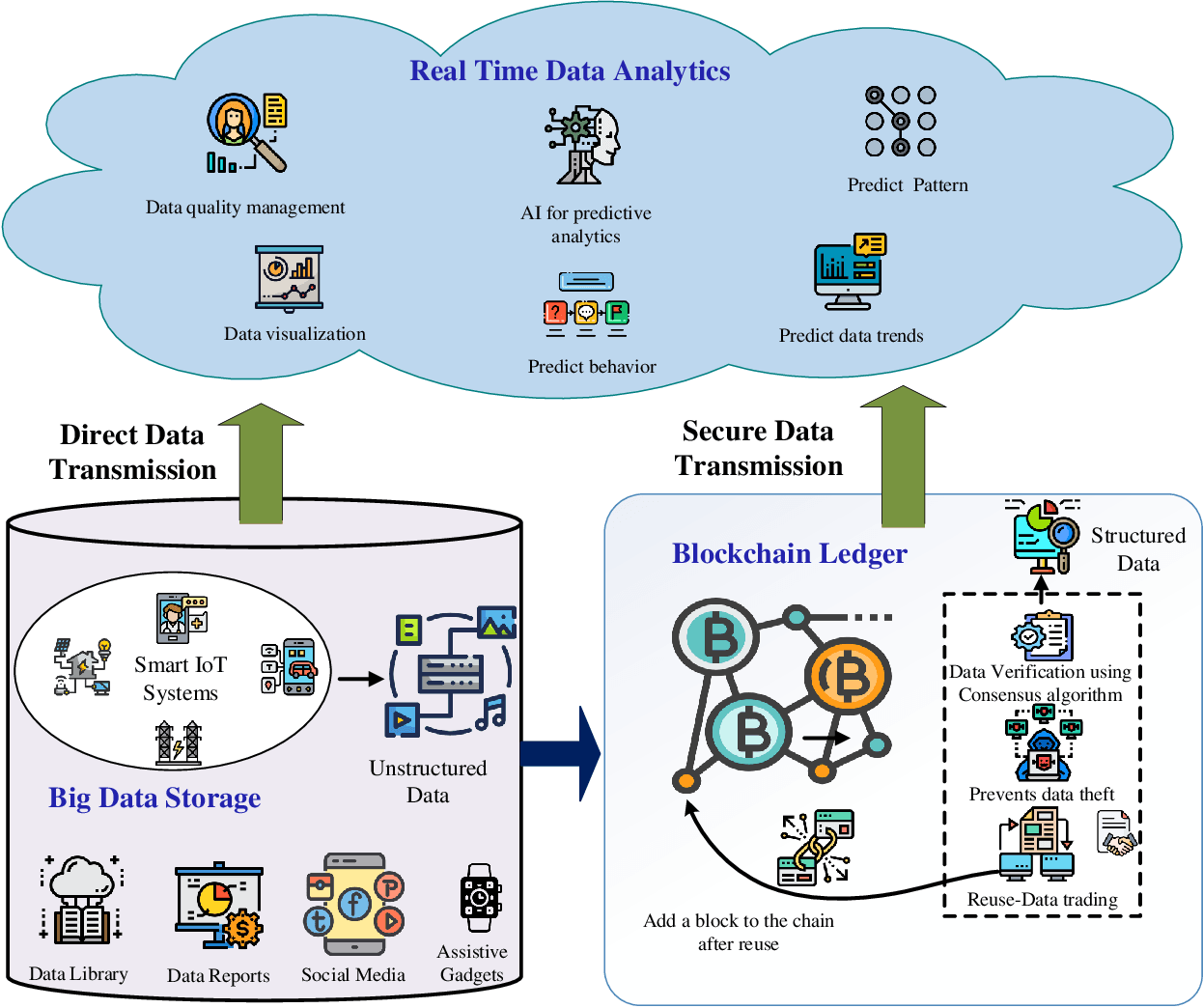

Many governments have run into trouble with blockchain anonymity provisions. Although favored for its security and accuracy, blockchain has been rejected due to its inability to track stakeholders in transactions, making it the preferred choice for illegal transactions. Big data applications can help make blockchains trackable by managing structured data sets of wallet addresses and their owner details. This infrastructure can convince governments to adopt blockchain as a trading platform that requires speed, security, reliability and traceability, all thanks to blockchain’s big data.

The close connection between blockchain and big data

Big Data can handle huge data sets with ease, but a number of issues in its infrastructure raise questions about the widespread adoption of the technology. Big Data infrastructure is centralized in one server location, providing complete and unconditional control of the data for those who access the server. This “ownership” becomes problematic when the Big Data infrastructure is shared between different companies, or between different regional offices of the same company. In addition, having multiple copies in different locations is not a solution, as it puts a burden on resources and creates confusion when determining the most up-to-date data resources.

In addition, as big data resources are traded between different entities, the legitimacy of the data resources raises concerns. With a blockchain for big data, we can create a decentralized data resource that is fully accessible to everyone. We can also track updates to data resources on the blockchain, thus eliminating the confusion caused by multiple copies. In addition, blockchain concepts such as proof of workload or proof of stake can be used to verify the legitimacy of data transactions, while blockchain can provide a robust financial platform for data transactions between entities.

The combination of big data and blockchain can significantly improve the usability of each other, and these technologies can help create a hybrid infrastructure with big data and blockchain as the backbone. The infrastructure will be flexible for different application types, such as its parents - big data and blockchain.